Market Watch

Snapshot of the Portuguese Economy: Mid-Year 2026 Update

|

|

Portugal enters the second half of 2026 with an economy that remains resilient but is clearly moving into a more demanding phase of the cycle. Growth is moderating, inflation has accelerated following the latest energy shock, and financial conditions are becoming less supportive. Even so, domestic demand, European funding, a robust labour market and improving balance sheets continue to provide meaningful support.

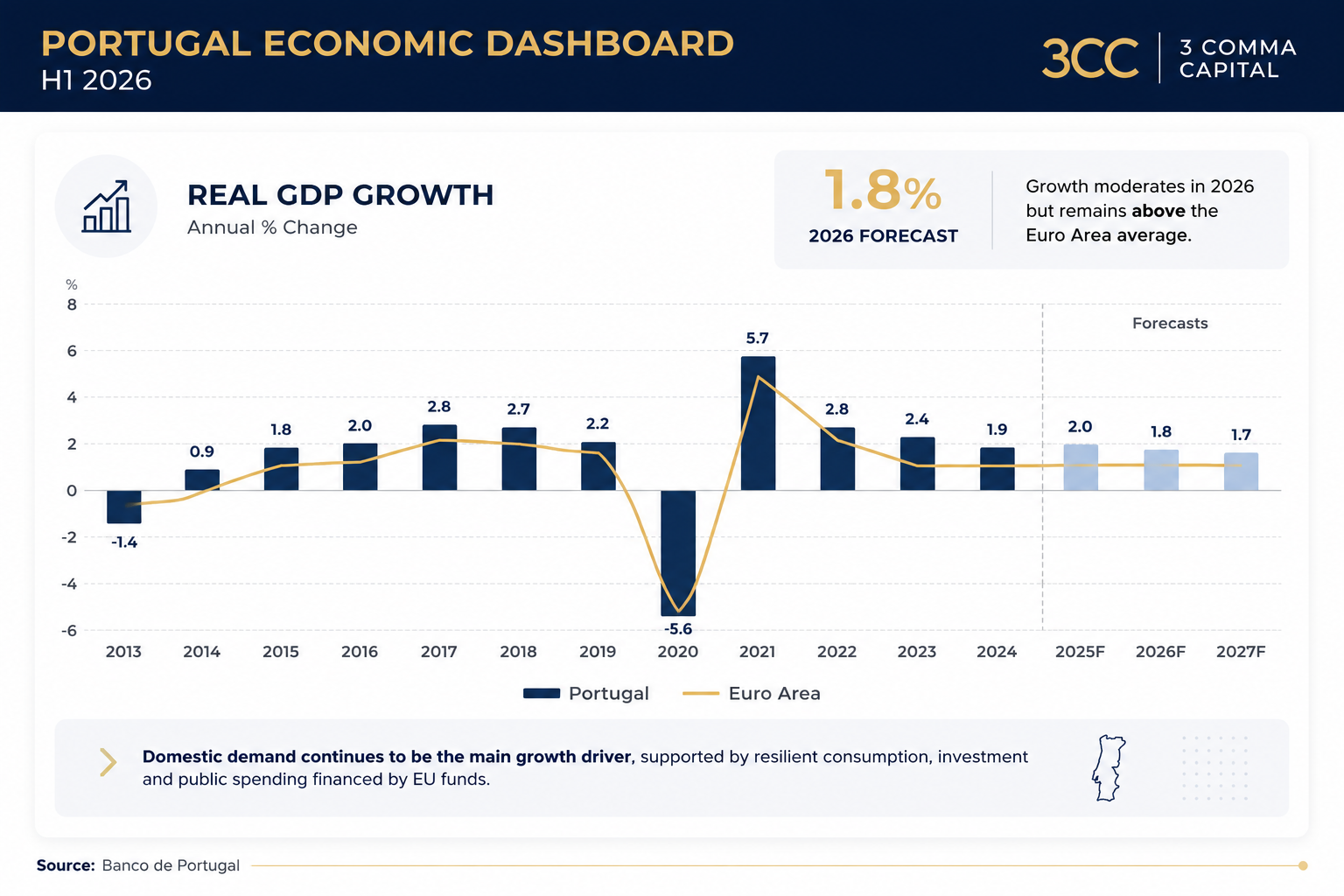

According to the Banco de Portugal’s June 2026 Economic Bulletin, Portuguese GDP is expected to grow by 1.8% in 2026, slow to 1.6% in 2027, and return to 1.8% in 2028. These projections are unchanged from March, although the composition of growth and the inflation outlook have become less favorable.

However, Banco de Portugal expects activity to recover during the remainder of the year, with moderate quarterly growth of approximately 0.4%. Domestic demand should remain the principal engine of expansion over the 2026–2028 period.

Private consumption is projected to rise by 1.9% in 2026, after increasing by 3.5% in 2025. The slowdown reflects weaker real income growth, higher energy costs, elevated uncertainty and less favorable financing conditions. Nevertheless, continued employment growth and accumulated household savings should help prevent a sharper deterioration in consumption.

Investment is expected to provide stronger support. Gross fixed capital formation is projected to grow by 4.5% in 2026, benefiting from peak implementation of the Recovery and Resilience Plan, public infrastructure projects and selected large private investments. Banco de Portugal specifically notes the contribution of a major data-centre investment in Sines, although its high import content limits its direct contribution to domestic value added.

This relative outperformance is supported by stronger domestic demand, continued inflows of European funds and a more favorable labour-market backdrop. However, the growth differential is expected to narrow over time as PRR-related investment fades and demographic constraints become more visible.

The structure of the Portuguese economy is also gradually changing. Services with higher technological and knowledge intensity are gaining weight in both gross value added and exports, helping to partially offset weaker momentum in more traditional sectors.

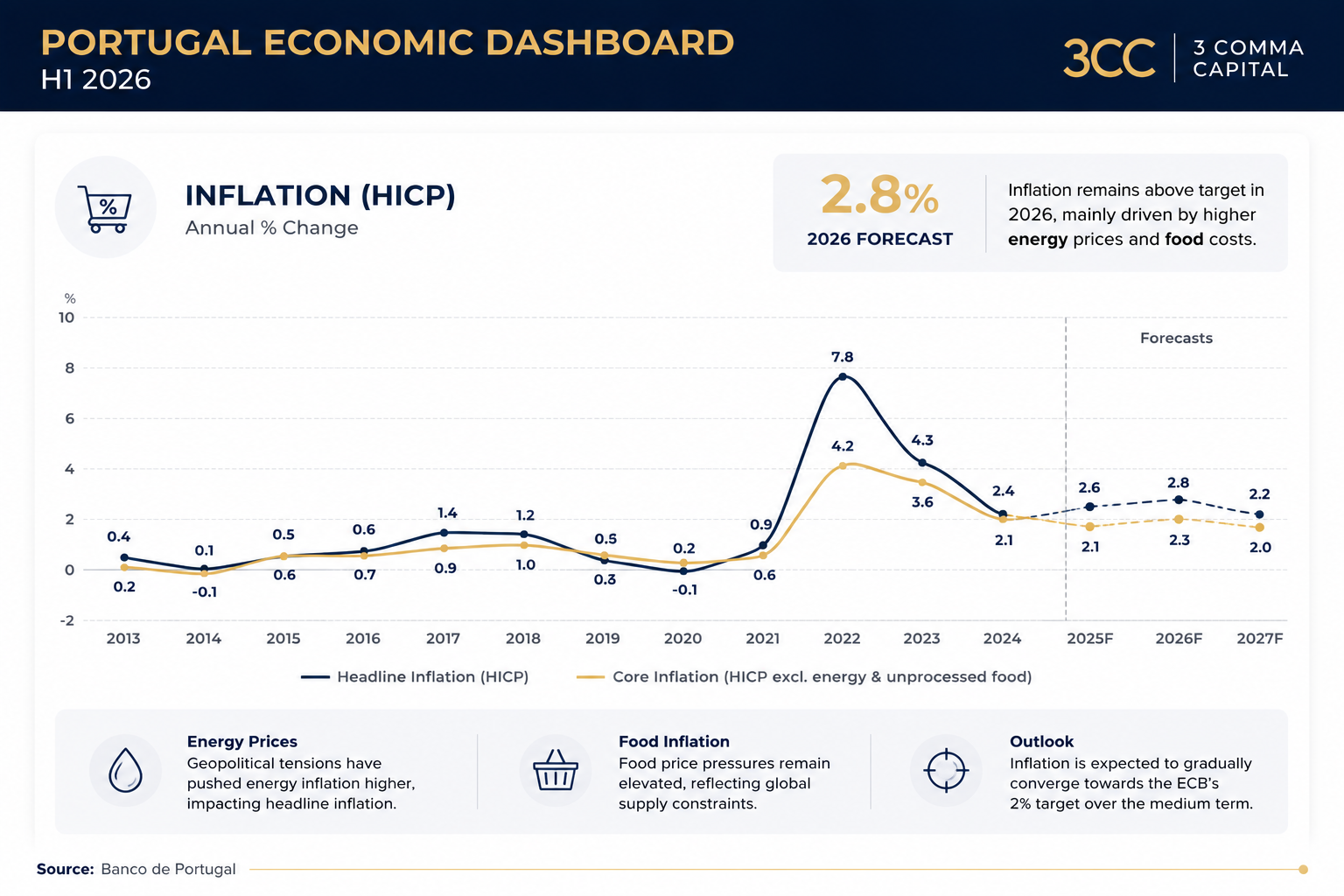

Banco de Portugal now expects the Harmonized Index of Consumer Prices to increase by 3.1% in 2026, up from the previous estimate of 2.8%. Inflation should then moderate to 2.4% in 2027 and return to 2.0% in 2028.

The revision largely reflects the sharp increase in oil prices associated with the conflict involving Iran. The Bank assumes that the shock will remain temporary and that oil prices will begin declining during the second half of 2026.

Core inflation is expected to remain more contained, at 2.4% in 2026, suggesting that the deterioration is predominantly external rather than the result of a broad-based reacceleration in domestic price pressures.

This distinction matters. A temporary energy shock reduces household purchasing power and increases business costs, but it is less damaging than a persistent wage-price spiral. The eventual easing of external pressures and more moderate labour-cost growth should allow inflation to move back towards the ECB’s target.

Banco de Portugal highlights three important structural improvements:

The financial position of households and companies has also strengthened. Relative to 2022, household debt declined by around 7 percentage points of GDP to 56%, while non-financial corporate debt fell by approximately 15 percentage points to 72%. Higher savings and lower leverage create a larger buffer against rising energy and financing costs.

This does not eliminate the risk, but it means that the Portuguese economy is better placed to withstand the current shock than it was during the 2022 energy crisis.

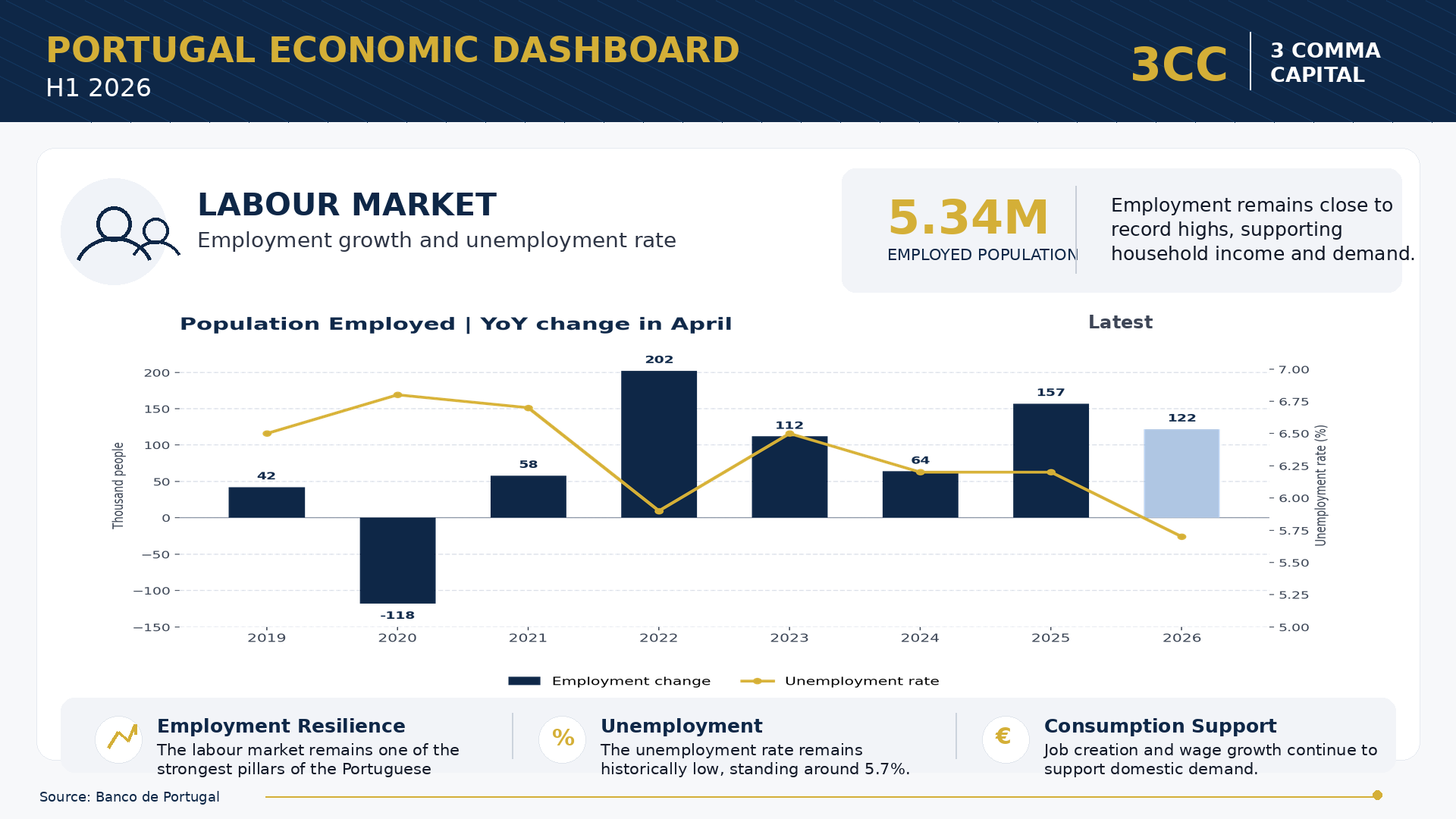

Employment is projected to grow by 1.0% in 2026, while the unemployment rate should remain close to historical lows at 5.9%. This combination continues to support household income, private consumption and confidence.

However, employment growth is expected to slow to 0.5% in 2027 and 0.4% in 2028. This is not primarily a sign of a cyclical downturn. Instead, it reflects increasingly binding supply constraints, including lower migration inflows, weaker population growth and a more limited expansion of the working-age population.

As a result, productivity will become increasingly important. Banco de Portugal expects GDP per worker to grow by 0.8% in 2026, 1.1% in 2027 and 1.4% in 2028, gradually replacing employment growth as the main source of economic expansion.

The final implementation phase of the PRR is expected to sustain investment in infrastructure, digitalization, energy transition and business modernization. Public investment and expansionary fiscal policy are therefore helping cushion the impact of weaker external demand and higher energy prices. (Banco de Portugal)

The picture becomes less favorable in 2027. The end of the PRR is expected to contribute to a sharp slowdown in fixed investment growth, from 4.5% in 2026 to only 1.1% in 2027.

This creates an important medium-term challenge. Portugal will need to translate the temporary boost from European funds into permanent improvements in productive capacity, technology adoption, skills and infrastructure.

Exports are expected to grow by 2.0% in 2026, compared with only 0.4% in 2025, but remain constrained by weak European growth, geopolitical uncertainty and a less favorable global trade environment. Imports are projected to rise by 3.7%, driven by domestic investment and consumption. (Banco de Portugal)

As a result, the balance of goods and services is expected to move from a surplus of 1.2% of GDP in 2025 to a small deficit of 0.2% in 2026. The broader current and capital account should remain in surplus at 2.7% of GDP, helped by European transfers.

Tourism remains an important source of external income, but future growth is likely to depend increasingly on higher-value services, technology-intensive activities and stronger export competitiveness rather than tourism alone.

After recording a budget surplus of 0.7% of GDP in 2025, Portugal is projected to post a small deficit of 0.2% in 2026, widening to 0.5% in 2027 and 2028. Even so, Portugal remains among the relatively small group of Euro Area countries with a budget position close to balance. (Banco de Portugal)

Public debt is expected to continue declining, from 89.7% of GDP in 2025 to 85.7% in 2026, and eventually to 79.5% in 2028. On this trajectory, Portuguese public debt would fall below the Euro Area average.

This is an important source of resilience, particularly in a world of higher interest rates and increased geopolitical risk. However, Banco de Portugal cautions that previously announced spending commitments and structural challenges make it essential to preserve fiscal space.

Under a more adverse scenario, the Banco de Portugal estimates that growth would be lower and inflation higher throughout the projection horizon. (Banco de Portugal)

Additional risks include weaker Euro Area demand, delays in PRR implementation and more binding demographic constraints.

Slower growth, higher inflation and more restrictive financing conditions argue against broad, indiscriminate risk-taking. At the same time, declining public debt, resilient domestic demand and a healthy labour market continue to support the creditworthiness of the Portuguese economy and many domestic issuers.

From an investment perspective, this environment reinforces the importance of:

Portugal’s medium-term investment case remains attractive, but returns are likely to depend increasingly on identifying the strongest issuers, sectors and structural growth themes.

The next phase of growth will depend less on employment expansion and fiscal support and more on productivity, investment, technology adoption and the successful transformation of European funding into lasting economic capacity.

Key Takeaways

- Portugal’s GDP is projected to grow by 1.8% in 2026, outperforming the Euro Area despite a weaker international environment.

- Domestic demand remains the main driver of growth, supported by consumption, investment and fiscal policy.

- Fixed investment is expected to rise by 4.5%, benefiting from the final phase of PRR implementation.

- Inflation has been revised higher to 3.1%, largely due to the external energy shock.

- Core inflation remains more contained, supporting the view that the latest acceleration is primarily temporary.

- The labour market remains resilient, with unemployment projected at 5.9%.

- Portugal is better prepared for an energy shock due to lower leverage, greater savings and increased renewable-energy penetration.

- Public debt is projected to decline below 80% of GDP by 2028, strengthening fiscal resilience.

- The main risks remain geopolitical, particularly a prolonged conflict and persistently higher energy prices.

- Future growth will depend increasingly on productivity, as employment and EU-fund growth lose momentum.

According to the Banco de Portugal’s June 2026 Economic Bulletin, Portuguese GDP is expected to grow by 1.8% in 2026, slow to 1.6% in 2027, and return to 1.8% in 2028. These projections are unchanged from March, although the composition of growth and the inflation outlook have become less favorable.

Portugal at a Glance

Growth Is Slowing, but Domestic Demand Remains Resilient

Portugal’s economy stagnated at the beginning of 2026, partly due to the fading impact of fiscal measures introduced in the second half of 2025 and partly because of adverse weather conditions. Private consumption was flat, tourism exports weakened and construction investment declined during the first quarter.However, Banco de Portugal expects activity to recover during the remainder of the year, with moderate quarterly growth of approximately 0.4%. Domestic demand should remain the principal engine of expansion over the 2026–2028 period.

Private consumption is projected to rise by 1.9% in 2026, after increasing by 3.5% in 2025. The slowdown reflects weaker real income growth, higher energy costs, elevated uncertainty and less favorable financing conditions. Nevertheless, continued employment growth and accumulated household savings should help prevent a sharper deterioration in consumption.

Investment is expected to provide stronger support. Gross fixed capital formation is projected to grow by 4.5% in 2026, benefiting from peak implementation of the Recovery and Resilience Plan, public infrastructure projects and selected large private investments. Banco de Portugal specifically notes the contribution of a major data-centre investment in Sines, although its high import content limits its direct contribution to domestic value added.

Real GDP Growth

Portugal Continues to Outperform the Euro Area

Portugal is still expected to grow faster than the Euro Area. Banco de Portugal projects Euro Area GDP growth of only 0.8% in 2026, compared with 1.8% for Portugal.This relative outperformance is supported by stronger domestic demand, continued inflows of European funds and a more favorable labour-market backdrop. However, the growth differential is expected to narrow over time as PRR-related investment fades and demographic constraints become more visible.

The structure of the Portuguese economy is also gradually changing. Services with higher technological and knowledge intensity are gaining weight in both gross value added and exports, helping to partially offset weaker momentum in more traditional sectors.

Inflation Has Reaccelerated

The most significant change since the March outlook is inflation.Banco de Portugal now expects the Harmonized Index of Consumer Prices to increase by 3.1% in 2026, up from the previous estimate of 2.8%. Inflation should then moderate to 2.4% in 2027 and return to 2.0% in 2028.

The revision largely reflects the sharp increase in oil prices associated with the conflict involving Iran. The Bank assumes that the shock will remain temporary and that oil prices will begin declining during the second half of 2026.

Core inflation is expected to remain more contained, at 2.4% in 2026, suggesting that the deterioration is predominantly external rather than the result of a broad-based reacceleration in domestic price pressures.

This distinction matters. A temporary energy shock reduces household purchasing power and increases business costs, but it is less damaging than a persistent wage-price spiral. The eventual easing of external pressures and more moderate labour-cost growth should allow inflation to move back towards the ECB’s target.

Inflation (HICP)

Better Prepared for an Energy Shock

Portugal remains exposed to imported energy, but its ability to absorb such a shock has improved materially since the beginning of the century.Banco de Portugal highlights three important structural improvements:

- Energy intensity has fallen by approximately one-third.

- External energy dependence declined to around 65% in 2024, down substantially from earlier levels.

- Renewable energy represented approximately 34% of primary energy needs and 79% of electricity generation in 2024.

The financial position of households and companies has also strengthened. Relative to 2022, household debt declined by around 7 percentage points of GDP to 56%, while non-financial corporate debt fell by approximately 15 percentage points to 72%. Higher savings and lower leverage create a larger buffer against rising energy and financing costs.

This does not eliminate the risk, but it means that the Portuguese economy is better placed to withstand the current shock than it was during the 2022 energy crisis.

Labour Market Remains a Key Source of Stability

The labour market continues to be one of Portugal’s strongest economic pillars.Employment is projected to grow by 1.0% in 2026, while the unemployment rate should remain close to historical lows at 5.9%. This combination continues to support household income, private consumption and confidence.

However, employment growth is expected to slow to 0.5% in 2027 and 0.4% in 2028. This is not primarily a sign of a cyclical downturn. Instead, it reflects increasingly binding supply constraints, including lower migration inflows, weaker population growth and a more limited expansion of the working-age population.

As a result, productivity will become increasingly important. Banco de Portugal expects GDP per worker to grow by 0.8% in 2026, 1.1% in 2027 and 1.4% in 2028, gradually replacing employment growth as the main source of economic expansion.

Labor Market

European Funds Continue to Support Investment

European funding remains a major support for Portugal in 2026.The final implementation phase of the PRR is expected to sustain investment in infrastructure, digitalization, energy transition and business modernization. Public investment and expansionary fiscal policy are therefore helping cushion the impact of weaker external demand and higher energy prices. (Banco de Portugal)

The picture becomes less favorable in 2027. The end of the PRR is expected to contribute to a sharp slowdown in fixed investment growth, from 4.5% in 2026 to only 1.1% in 2027.

This creates an important medium-term challenge. Portugal will need to translate the temporary boost from European funds into permanent improvements in productive capacity, technology adoption, skills and infrastructure.

External Demand Is the Weakest Part of the Outlook

Portugal’s external sector is facing a more difficult environment.Exports are expected to grow by 2.0% in 2026, compared with only 0.4% in 2025, but remain constrained by weak European growth, geopolitical uncertainty and a less favorable global trade environment. Imports are projected to rise by 3.7%, driven by domestic investment and consumption. (Banco de Portugal)

As a result, the balance of goods and services is expected to move from a surplus of 1.2% of GDP in 2025 to a small deficit of 0.2% in 2026. The broader current and capital account should remain in surplus at 2.7% of GDP, helped by European transfers.

Tourism remains an important source of external income, but future growth is likely to depend increasingly on higher-value services, technology-intensive activities and stronger export competitiveness rather than tourism alone.

Fiscal Policy Remains Supportive, but Discipline Still Matters

Fiscal policy is expected to remain expansionary throughout the projection period.After recording a budget surplus of 0.7% of GDP in 2025, Portugal is projected to post a small deficit of 0.2% in 2026, widening to 0.5% in 2027 and 2028. Even so, Portugal remains among the relatively small group of Euro Area countries with a budget position close to balance. (Banco de Portugal)

Public debt is expected to continue declining, from 89.7% of GDP in 2025 to 85.7% in 2026, and eventually to 79.5% in 2028. On this trajectory, Portuguese public debt would fall below the Euro Area average.

This is an important source of resilience, particularly in a world of higher interest rates and increased geopolitical risk. However, Banco de Portugal cautions that previously announced spending commitments and structural challenges make it essential to preserve fiscal space.

Risks Have Become More Asymmetric

The outlook remains subject to unusually high uncertainty.Downside Risks

The principal risk is a longer or more intense conflict in the Middle East. This could produce:- higher and more persistent energy prices;

- renewed supply-chain disruption;

- increased financial-market volatility;

- weaker business and consumer confidence;

- more restrictive monetary and financial conditions.

Under a more adverse scenario, the Banco de Portugal estimates that growth would be lower and inflation higher throughout the projection horizon. (Banco de Portugal)

Additional risks include weaker Euro Area demand, delays in PRR implementation and more binding demographic constraints.

Potential Upside Factors

The outlook could improve if:- the energy shock unwinds faster than anticipated;

- EU funds are executed more efficiently;

- public and private investment accelerates;

- digital infrastructure and AI-related projects generate stronger productivity gains;

- Portugal continues to expand its presence in higher-value service exports.

What This Means for Investors

The Portuguese macroeconomic backdrop remains constructive, but it is increasingly selective.Slower growth, higher inflation and more restrictive financing conditions argue against broad, indiscriminate risk-taking. At the same time, declining public debt, resilient domestic demand and a healthy labour market continue to support the creditworthiness of the Portuguese economy and many domestic issuers.

From an investment perspective, this environment reinforces the importance of:

- quality fixed income, particularly where yields compensate investors for duration and credit risk;

- active credit selection, rather than passive exposure to the entire market;

- selective equity exposure to companies benefiting from domestic investment, digitalization and infrastructure spending;

- diversification, given the continued sensitivity of the economy to energy prices and external demand;

- productivity-linked investment themes, including technology, data infrastructure and higher-value services.

Portugal’s medium-term investment case remains attractive, but returns are likely to depend increasingly on identifying the strongest issuers, sectors and structural growth themes.

► Bottom Line

Portugal enters the second half of 2026 with slower growth, temporarily higher inflation and greater external uncertainty, but also with stronger structural foundations than in previous cycles. A resilient labour market, substantial European funding, improving balance sheets and falling public debt continue to distinguish Portugal from many of its European peers.The next phase of growth will depend less on employment expansion and fiscal support and more on productivity, investment, technology adoption and the successful transformation of European funding into lasting economic capacity.

|

Investments Principal

|

With more than 20 years of experience in financial markets, Duarte specialized in the energy area in the last decade, where he had the opportunity to work with the main European Power and Gas institutions at CIMD Group. Previously, he worked as Market Strategist at IG Markets Iberia.

More about Duarte Caldas