Market Watch

S&P 500 Valuations: Strong Earnings vs. Rising Real Yields

|

|

Key Takeaways

- The U.S. economy remains remarkably resilient, with GDP growth and corporate earnings continuing to surprise positively.

- S&P 500 valuations remain historically elevated, trading around 20.9x forward earnings, well above long-term averages.

- Forward earnings growth expectations above 20% are helping justify current market levels.

- Rising real interest rates are becoming the primary headwind for equities, pressuring valuation multiples and increasing the cost of capital.

- The U.S. Equity Risk Premium remains historically low, suggesting equities are less attractive relative to bonds than in previous years.

- European equities currently appear cheaper than U.S. equities, both on P/E and ERP metrics.

- AI-driven optimism continues to support market leadership and elevated multiples, particularly among mega-cap technology stocks.

- The market environment remains constructive but increasingly fragile, with higher sensitivity to inflation, bond yields, and earnings disappointments.

► Bottom Line:

The S&P 500 continues to trade at elevated valuations because earnings growth remains exceptionally strong. However, rising real interest rates are increasingly challenging further multiple expansion and making bonds more competitive relative to equities. The next phase of the market will likely depend less on liquidity and more on whether earnings growth can continue to outpace the pressure from higher real yields.

The U.S. equity market continues to challenge traditional valuation frameworks. Despite elevated interest rates, persistent inflation concerns, and geopolitical uncertainty, the S&P 500 remains near record levels, supported by resilient economic growth and robust corporate earnings.

Yet beneath the surface, a more nuanced picture is emerging. The current market environment is increasingly defined by a tug-of-war between two opposing forces: strong earnings momentum and rising real interest rates.

The result is a market where valuations remain historically elevated, but where the expansion of multiples is becoming increasingly difficult.

The U.S. Economy Refuses to Slow Down

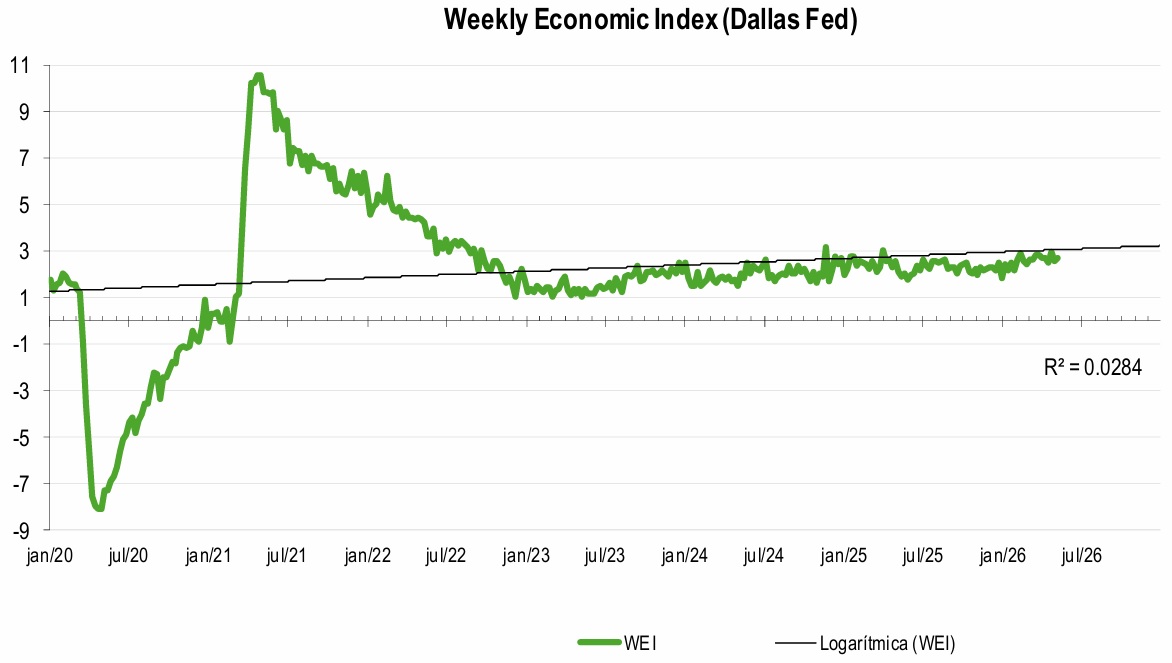

One of the key reasons behind the resilience of U.S. equities is simple: the economy continues to perform remarkably well.The Dallas Fed Weekly Economic Index remains aligned with long-term expansion trends:

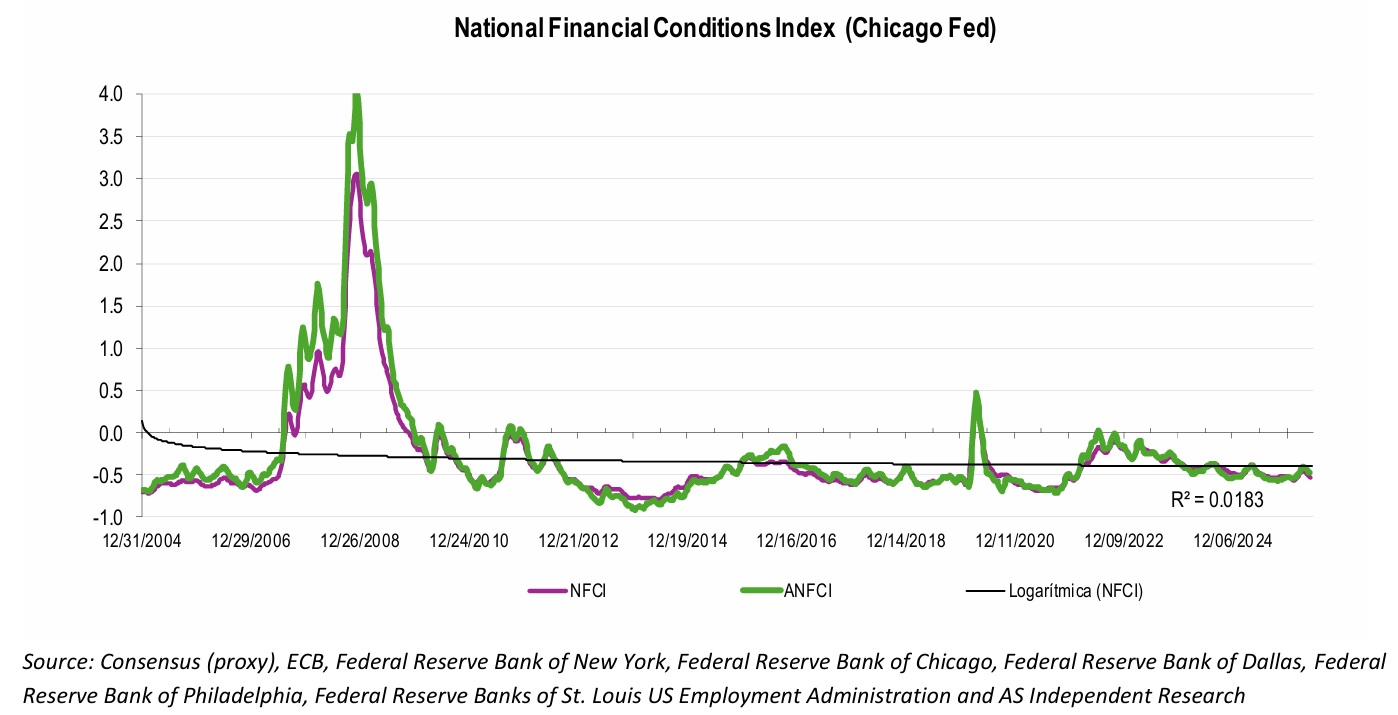

Financial conditions, measured by the Chicago Fed NFCI, have improved in recent weeks:

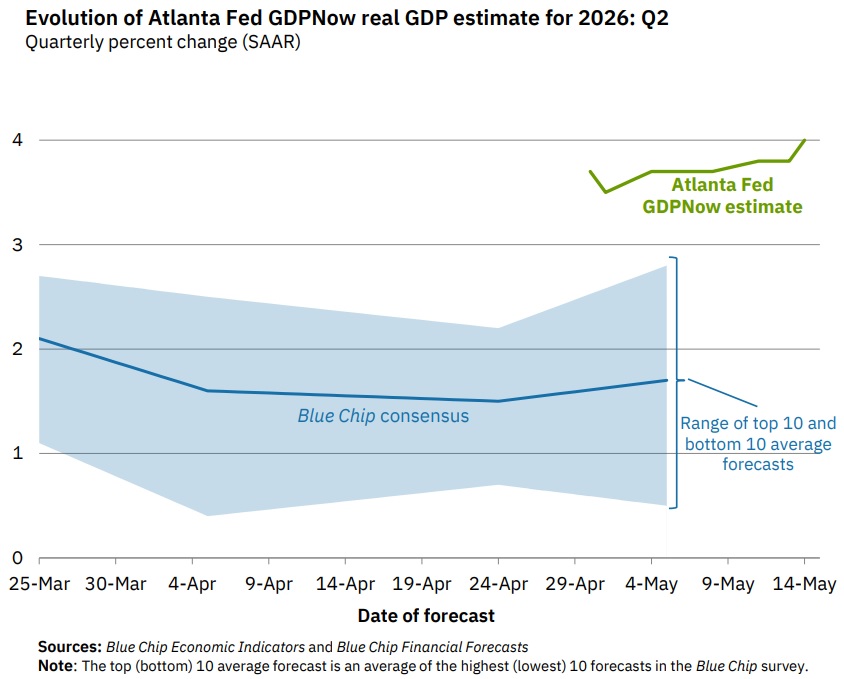

The Atlanta Fed GDPNow model recently pointed toward approximately 4% GDP growth for Q2 2026:

In other words, despite higher rates and tighter monetary conditions compared to previous years, the U.S. economy continues to display significant resilience. This strength is also feeding directly into earnings expectations.

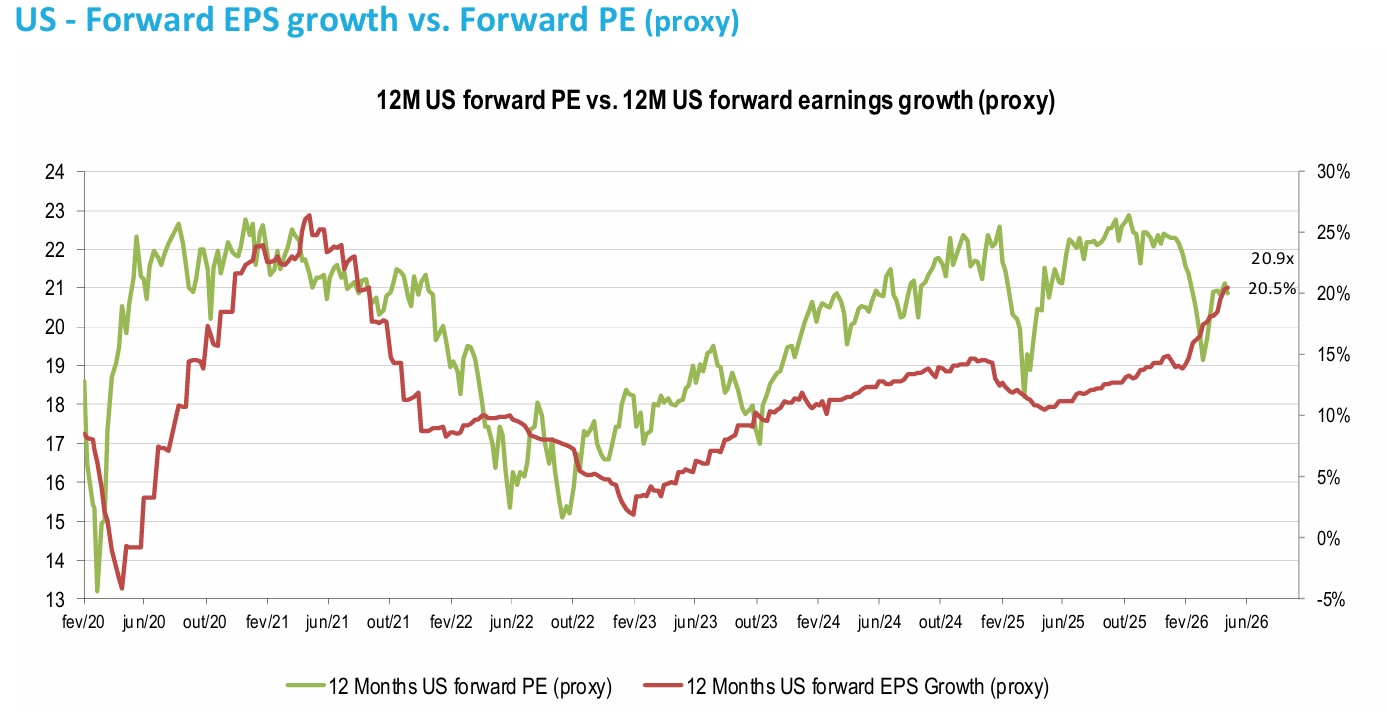

Forward earnings estimates for the S&P 500 continue to be revised upward, with forward EPS growth expectations now exceeding 20%.

That earnings strength is helping justify elevated equity prices - for now.

Valuations Remain Historically Elevated

The S&P 500 currently trades at approximately 20.9x forward earnings, slightly below recent peaks but still well above long-term historical averages.To put this into perspective:

- The 20-year average forward P/E is roughly 16.4x

- The 10-year average sits near 18.9x

- The 5-year average is around 19.8x

This means the market remains expensive relative to history, even after accounting for the extraordinary earnings growth currently being delivered by large U.S. corporates. However, unlike previous speculative episodes, today’s valuations are not being driven purely by optimism or liquidity. The earnings backdrop is materially stronger.

This distinction matters.

The Real Problem: Rising Real Yields

The biggest headwind for equities today is not necessarily earnings, it is the sharp increase in real interest rates:- U.S. 10-year Treasury yields recently climbed to approximately 4.6%

- Core inflation stands near 2.8%

- This places real long-term yields around 1.8%, close to the highest levels seen in decades.

Historically, higher real yields create a difficult environment for equities because they:

- Increase the discount rate applied to future earnings

- Raise the cost of capital

- Pressure valuation multiples downward

- Tighten overall financial conditions over time

In practical terms, investors can now earn materially positive real returns from government bonds again, something largely absent during the ultra-low-rate era of the 2010s.

This creates direct competition for equities.

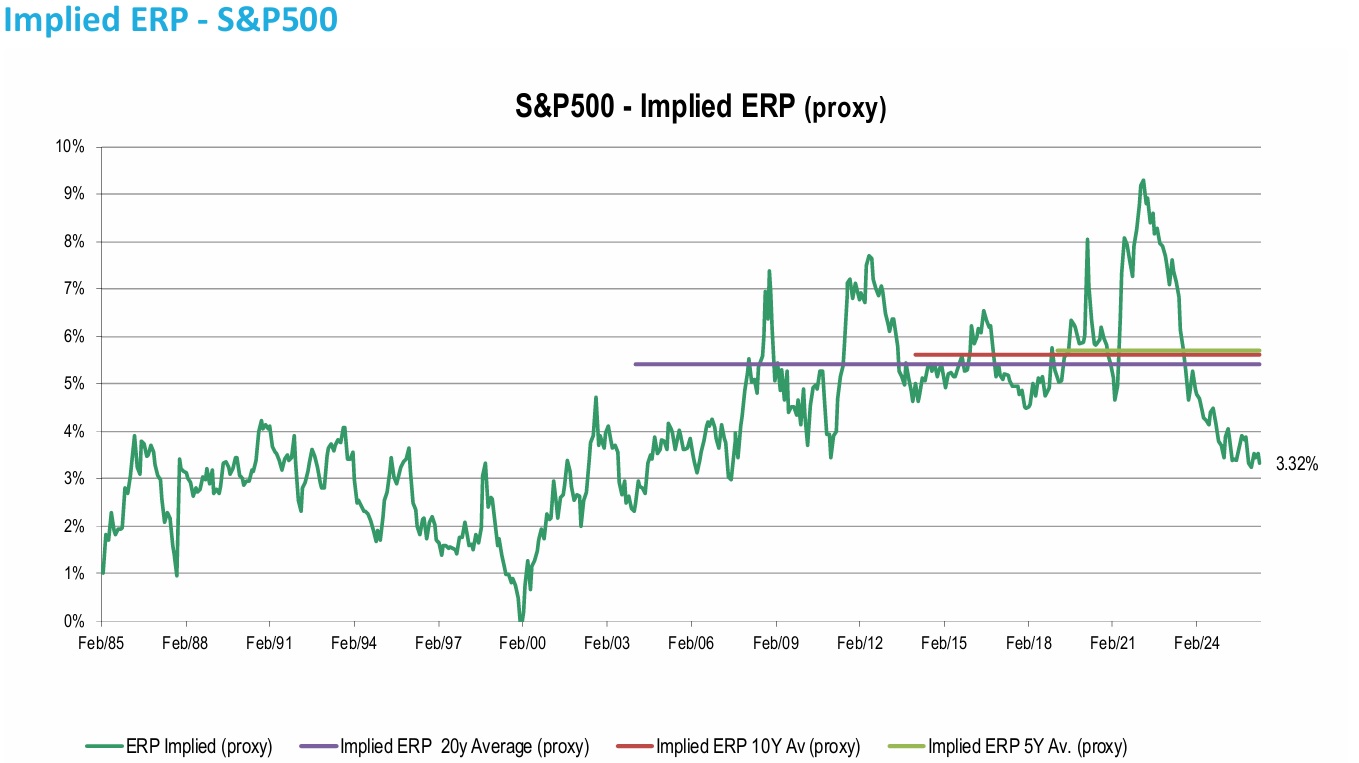

Equity Risk Premium Signals Caution

One of the most important valuation indicators is the Equity Risk Premium (ERP), which measures the additional return investors receive for owning equities over risk-free bonds. Currently, the implied U.S. ERP sits around 3.32%, significantly below long-term averages near 5.4%. This places the U.S. equity market firmly in “Unattractive” valuation region.

- Stocks are not necessarily overvalued because earnings are weak

- Stocks appear expensive because bond yields have become far more attractive

That distinction helps explain why multiples have stopped expanding, even as earnings continue to improve.

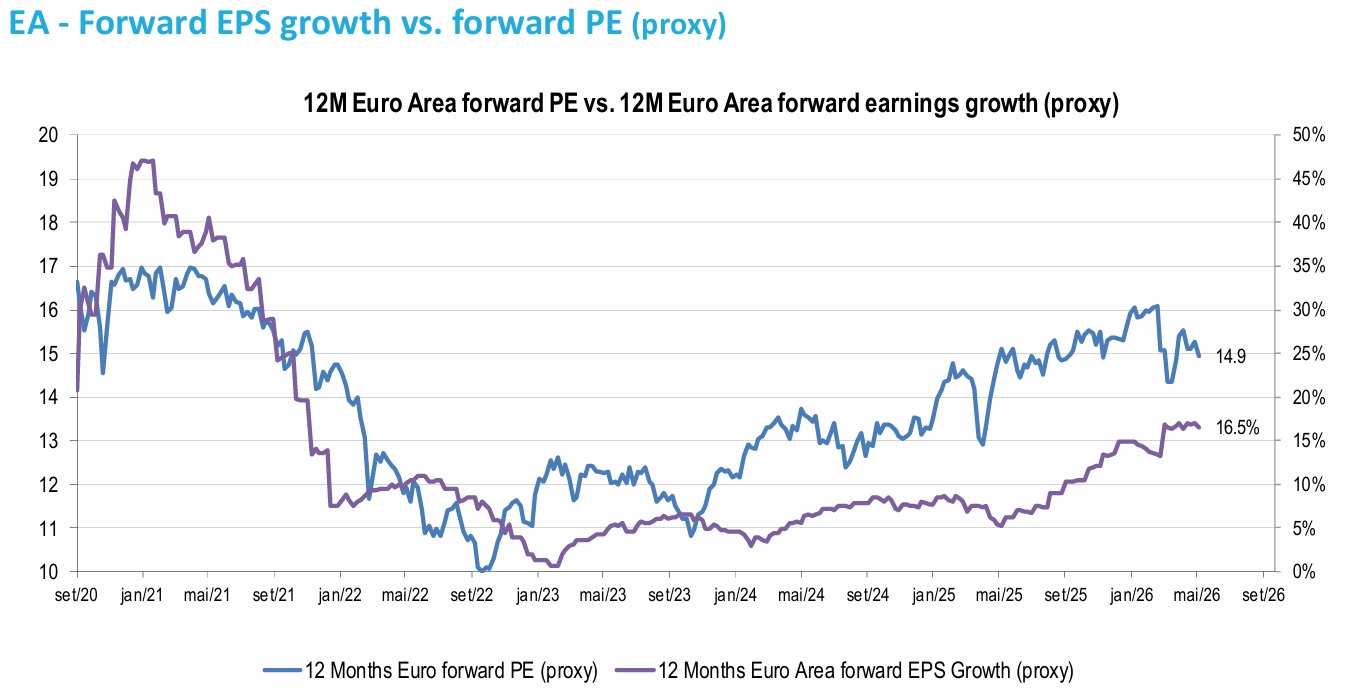

Europe Looks Relatively More Attractive

Interestingly, valuation dynamics in Europe currently appear more favorable than in the United States:

The Euro Area:

- Trades at approximately 14.9x forward earnings

- Maintains a materially higher ERP of roughly 5.14%

- Offers lower valuation multiples alongside improving earnings expectations.

This relative gap between U.S. and European valuations has widened significantly over the last decade, largely driven by the dominance of U.S. technology companies and AI-related optimism. However, if higher real yields persist, investors may increasingly question whether the valuation premium of U.S. equities remains fully justified.

AI Optimism Is Supporting Multiples

Another critical factor supporting the S&P 500 is the ongoing AI investment cycle. The market continues to assign premium valuations to companies exposed to:- Artificial Intelligence infrastructure

- Semiconductors

- Cloud computing

- Automation

- Digital productivity

Much like previous transformational technology cycles, investors are willing to pay elevated multiples for companies perceived as long-term structural winners. This dynamic helps explain why the market continues to trade near historical highs despite macro headwinds. However, it also creates concentration risk.

A relatively small group of mega-cap technology stocks continues to drive a disproportionate share of index performance.

The Market Environment Is Becoming More Fragile

The current setup is not necessarily bearish, but it is becoming increasingly delicate. Strong earnings continue to support equities, but rising real yields are simultaneously pressuring valuations. This creates a market environment where:- Earnings misses could be punished more aggressively

- Inflation surprises matter more

- Bond market volatility becomes increasingly important

- Liquidity conditions may tighten further if oil prices remain elevated

All in all, higher real yields historically tend to slow economic activity over time while simultaneously increasing the Cost of Equity - a negative combination for risk assets.

|

Investments Principal

|

With more than 20 years of experience in financial markets, Duarte specialized in the energy area in the last decade, where he had the opportunity to work with the main European Power and Gas institutions at CIMD Group. Previously, he worked as Market Strategist at IG Markets Iberia.

More about Duarte Caldas